Markets caught in cross-currents

Markets were pulled in different directions during the period under review.1 Long-term government bond yields in core markets rose despite easing monetary policies, tightening financial conditions. In contrast, corporate credit remained buoyant, equity valuations stayed elevated and US dollar appreciation halted. This resulted in easier conditions despite the uncertain outlook, which seemed not fully priced in financial markets. Sentiment towards emerging market economies (EMEs) remained subdued, as investors struggled to ascertain their outlook amid diverse domestic conditions and global policy uncertainty.

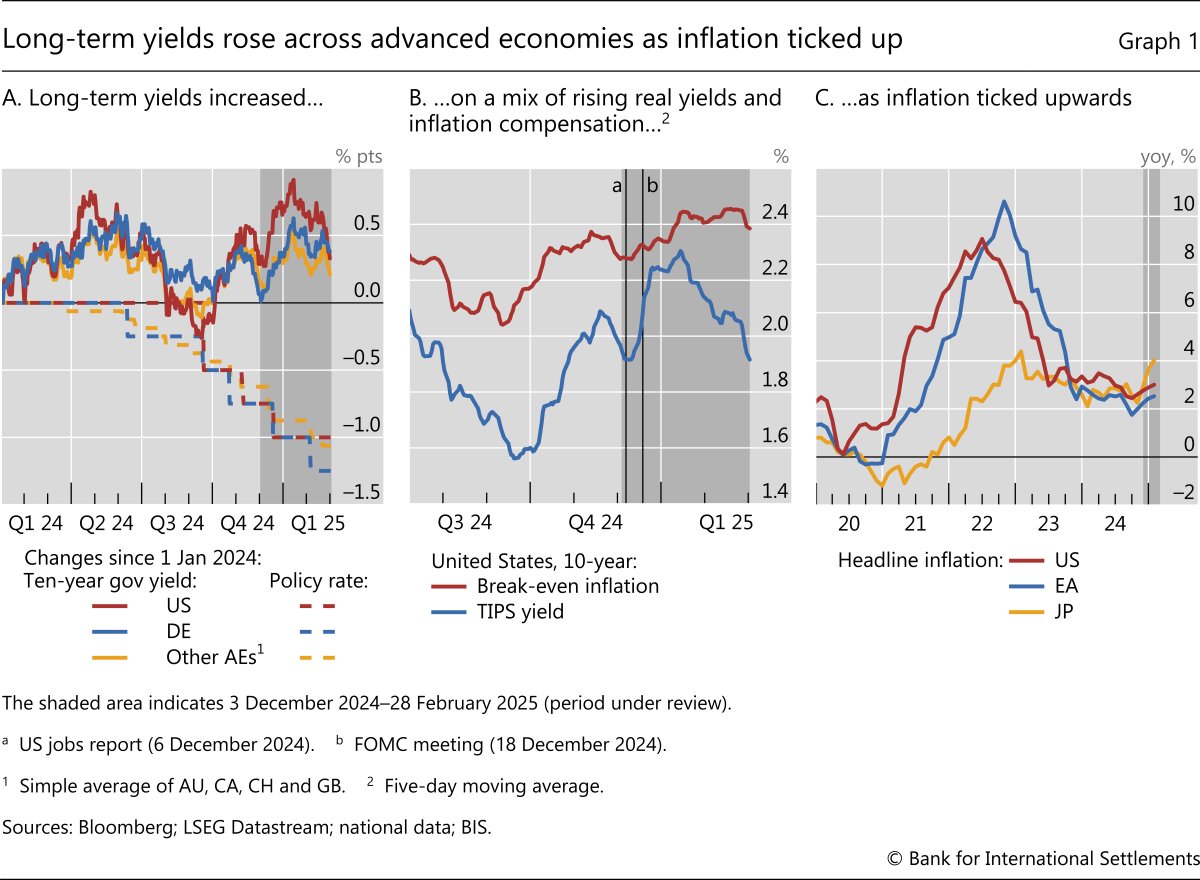

While policy rates came down, long-term yields generally rose across major economies. The upward shift was initially driven by US yields and spilled over to other major markets. The moves went alongside large swings in real yields – spearheaded by term premia, shifts in market-based gauges of neutral rates and, in some jurisdictions, uncertainty about the fiscal outlook. Indeed, heightened investor unease with abundant bond supply seemed to add to the pressures of diminishing risk-insensitive demand, as quantitative tightening continued. Overall, yield curves in major economies thus steepened further and were solidly upward-sloping. Yet, although the rise in the 10-year US benchmark largely reversed late in the review period, long yields in other jurisdictions remained at significantly higher levels.

Irrespective of the bond market ebbs and flows, and brief episodes of heightened volatility, risky assets exhibited resilience across AEs. Risk-taking was especially pronounced in corporate credit markets, with credit spreads narrowing further, particularly in Europe. Leveraged loans and private credit continued to pick up pace on the back of resurgent leveraged buyout (LBO) and merger and acquisition (M&A) activity. Stock markets in most advanced economies (AEs) traded sideways but stayed at relatively high valuations. European stocks surprised with a vigorous rally, outperforming most other markets on the back of markedly improved sentiment. A few jitters in the wake of AI-related developments and key policy announcements, including on tariffs, were not enough to derail the predominantly positive sentiment.

Financial conditions were more mixed across EMEs, but the overall sentiment was subdued. Headwinds seemed to gather strength from a pause in the Federal Reserve's easing trajectory, uncertainty with regard to US trade policy and a still struggling Chinese economy. While the breather in the US dollar appreciation provided some relief, local currency government bond yields lingered at elevated levels. Yields rose sharply in some economies where fiscal concerns came into investors' focus. Conditions in stock markets differed across countries. Chinese equities staged a rally late in the review period, driven mainly by technology stocks, while others saw tepid performance, despite a few bright spots that emerged in regional stock markets. Sentiment was lukewarm, however, reflected in anaemic portfolio flows that essentially drew to a standstill.

Key takeaways

- Despite policy easing, long-term government bond yields saw upward pressure across advanced economies, with fluctuations in real yields and term premia as the biggest drivers of yield moves.

- Risky assets exhibited resilience despite brief bouts of volatility and lingering concerns over tariffs, with robust risk-taking in corporate credit and European stocks.

- Sentiment was subdued in emerging market economies, as investors struggled to gauge the outlook for them amid varied domestic conditions and global policy uncertainty.

Long-term yields rise amid wide fluctuations

Bond markets reflected most clearly the cross-currents of uncertainty. Long-term yields whipsawed in AEs but finished the review period higher despite policy easing by major central banks. The swings in bond yields largely owed to fluctuating real yields amid an upward drift in inflation compensation. In some countries, the upward move was bolstered by unfavourable market dynamics and heightened investor unease with fiscal outlooks.

Central banks in major economies continued on their path of policy easing during the review period, but with varying outlooks. The Federal Reserve cut its policy rate by 25 basis points in December but signalled fewer rate cuts in 2025, as the economy and labour market looked robust (Graph 1.A, dashed red line). Other central banks, including the Bank of England and Sveriges Riksbank, also hinted at a pause in policy easing. The ECB, however, lowered policy rates and indicated that further cuts might be needed in the light of slower than expected growth. In contrast, the Bank of Japan raised rates once again, as it continued with its process of policy normalisation. These policy moves, and expectations thereof, were reflected in a downward trend in short-term rates.

In contrast to short-term rates, long rates soared in December, initially boosted by strong macroeconomic data. In the United States, 10-year yields rose by more than 60 basis points before largely retracing that surge from mid-January onwards (Graph 1.A, solid red line). These swings in long-term rates were driven by real yields, while inflation compensation edged up during the period (Graph 1.B). Inflation readings across major economies stayed above target throughout 2024 and ticked up at year-end (Graph 1.C). The persistence of inflation, together with the resilience of labour markets, particularly in the United States, pushed rates higher as investors reassessed the prospects of a prolonged period of higher policy rates. In this market environment, the rise in US yields pulled up those in other major economies early in the review period (Box A). As US yields subsequently came down in February, rates in other major economies traded sideways.

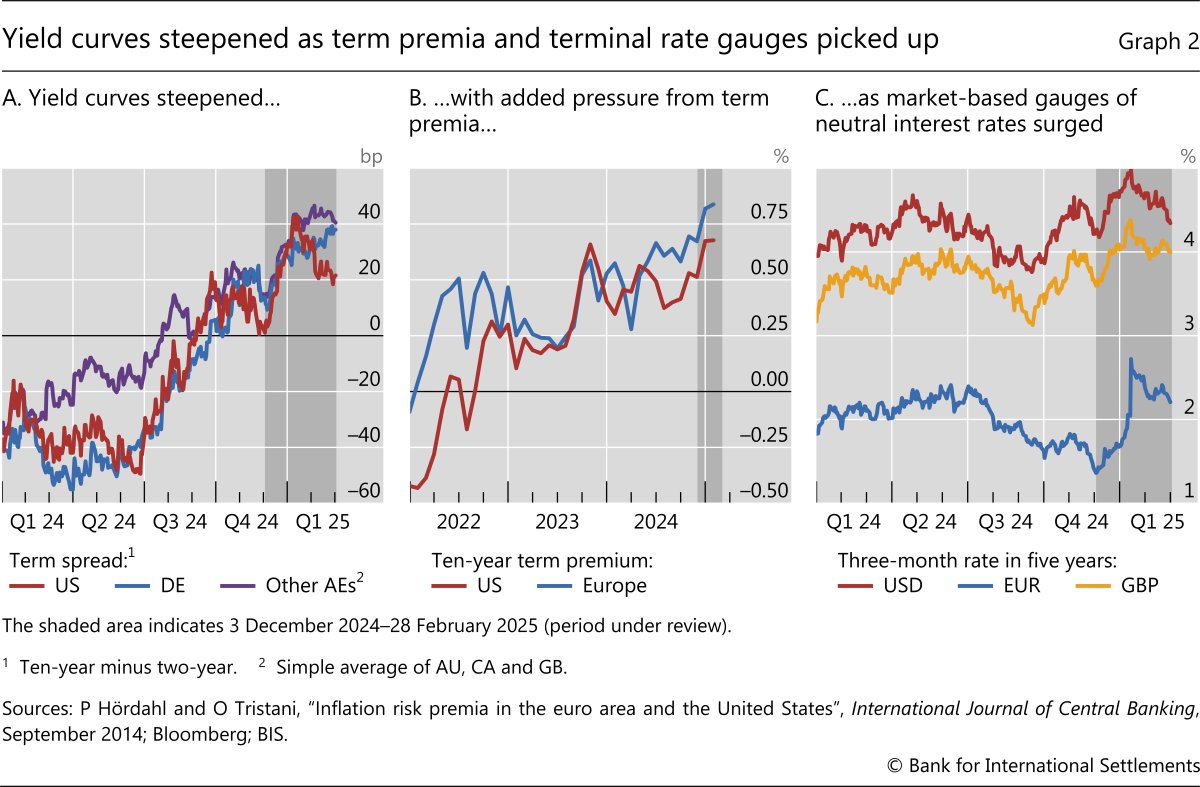

The rise of long-term rates led to a material steepening of yield curves. Term spreads turned solidly positive in most AEs, particularly in non-US markets (Graph 2.A). The yield curve steepening was exacerbated by a notable increase in term premia (Graph 2.B), indicating that investors demanded greater compensation for holding long-term interest rate exposure. Moreover, market-based gauges of neutral interest rates also rose steadily throughout the review period, and especially sharply for the euro area (Graph 2.C).

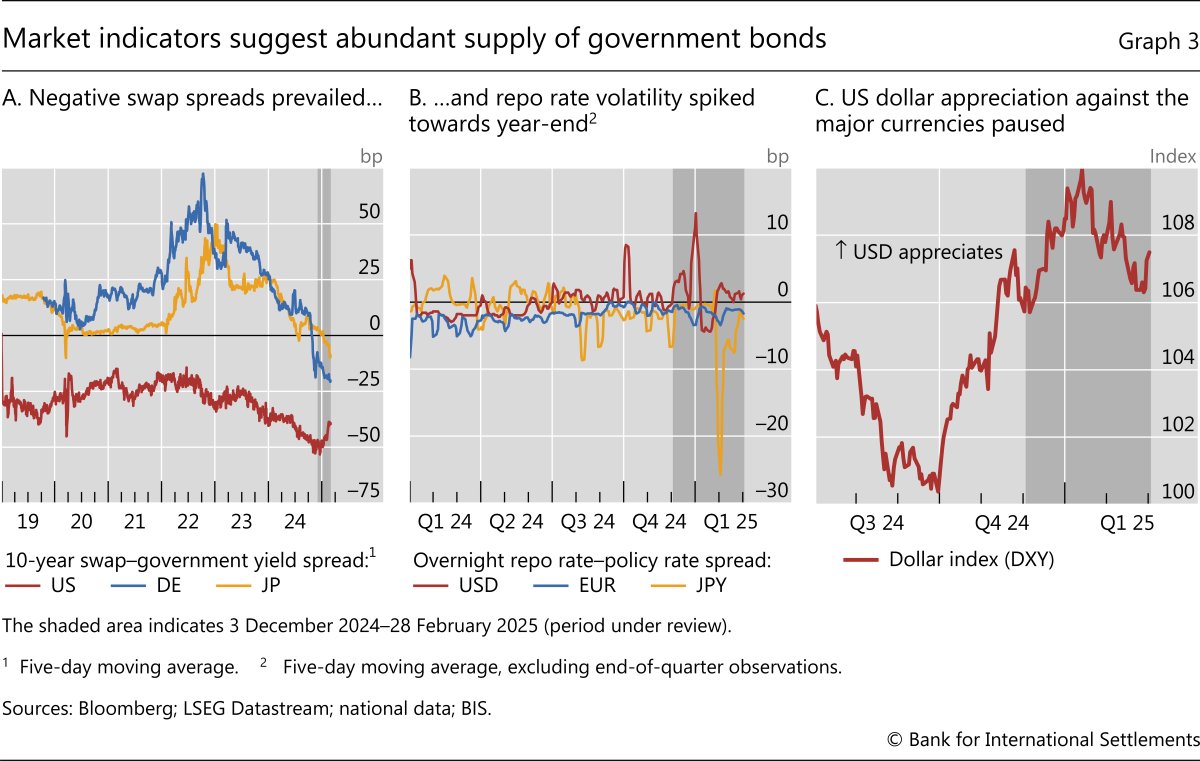

The increase in term premia coincided with market signals of abundant government bond supply. For instance, interest rate swap spreads – the difference between the fixed rate leg of an interest rate swap and government bond yields of the same tenor – turned negative for Japanese yen swaps during the review period, joining comparable US and German instruments (Graph 3.A). Swap spreads have been negative in the United States for a prolonged time, but touched multi-year lows during the review period.2

Short-term funding markets in the United States also reflected the influence of more abundant bond collateral, in combination with typical year-end constraints on dealer intermediation. The spread between the US overnight repo rate and the effective federal funds rate experienced a significant spike towards the end of 2024 (Graph 3.B, red line). This spike appeared to reflect the heightened need for repo financing to accommodate large Treasury issuances and constraints on dealers' balance sheet space due to end-of-year regulatory reporting requirements. No such jumps were observed in Europe or Japan (blue and yellow lines, respectively), where bond collateral at this juncture seems relatively less abundant.

The appreciation of the US dollar peaked and then reversed during the review period. While the greenback gained some additional ground in December, reaching its highest parity since late 2022, it retraced its path from mid-January as doubts about the US growth outlook began to mount (Graph 3.C). This turnaround was not uniform across currencies, as some commodity currencies and the yen still depreciated further.

Pricing of risky assets remains in hot territory

Risky asset markets remained resilient during the review period, shrugging off uncertainties about the outlook. Buoyant credit markets and elevated equity valuations countervailed the pressure from rising long-term bond yields, contributing to an easing of financial conditions in AEs.

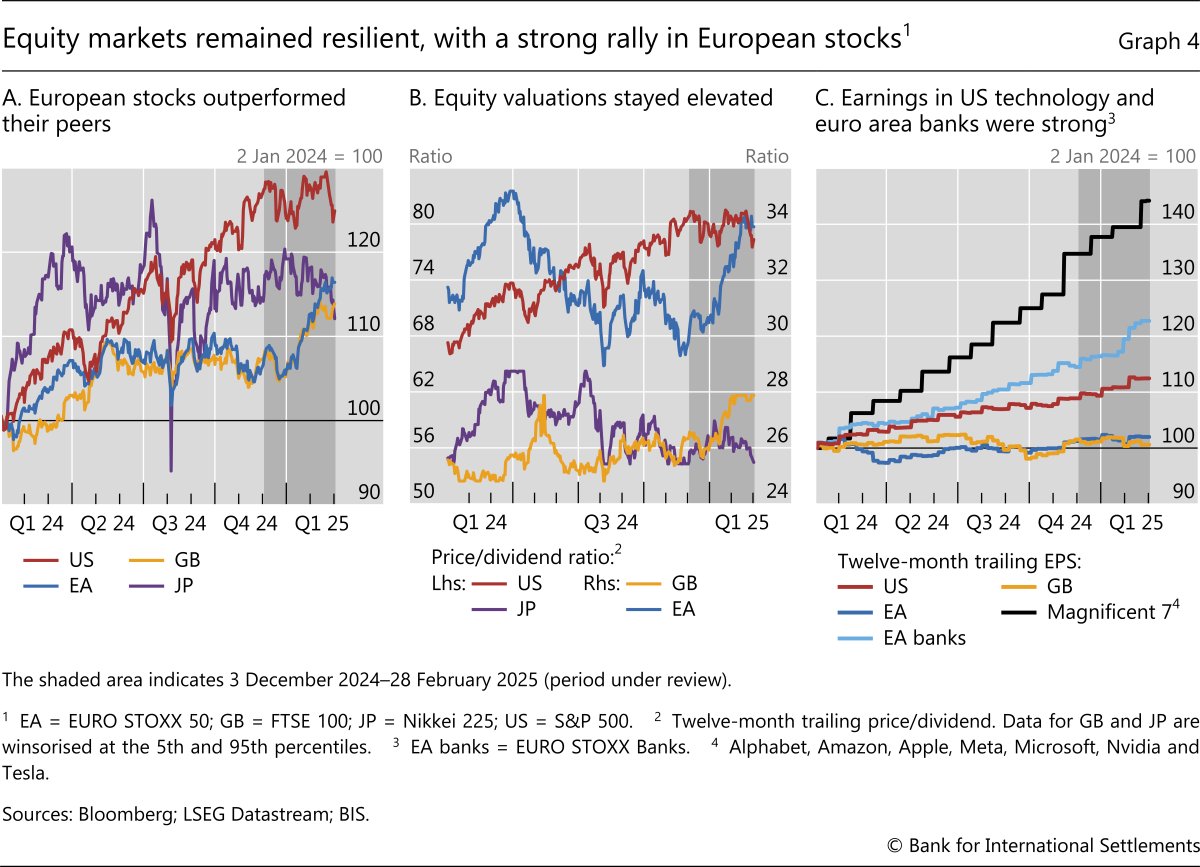

Risk sentiment in equity markets remained largely intact, even though the performance of individual markets varied across major economies. European stocks surprised with a strong rally and outperformed US equities, which traded sideways like those of most other jurisdictions (Graph 4.A). Accordingly, valuations (as measured here by price/dividend ratios) remained elevated in the United States and increased materially in Europe (Graph 4.B). US market valuations were supported by strong earnings, particularly from technology firms (Graph 4.C). These companies performed well and sustained the US market, while the post-election surge in small cap stocks faded away. Across the Atlantic, investors shrugged off weaker than expected earnings, consistent with relatively weaker economies. The surge appeared driven by a large compression of the European equity risk premium and by the strong rally of banks – whose earnings continued showing strength – and other sectors that had been particularly shaken in the first quarter of 2022 (Box B).

Despite the solid equity performance in most AEs, bouts of volatility returned briefly during the period. The VIX spiked in the wake of the Federal Open Market Committee meeting in December, increasing by more than 70% on the day of the policy decision announcement. The substantial jump in volatility underscored the swift and pronounced market response to a reassessment of beliefs about the monetary policy path ahead. However, the increase was short-lived as contrarian investors and sellers of volatility presumably dampened the move. Markets were also jittery in late January on the back of risk-off sentiment related to artificial intelligence (AI) and in late February to early March on deteriorating investor confidence following a softening of growth signals and tariff-related news.

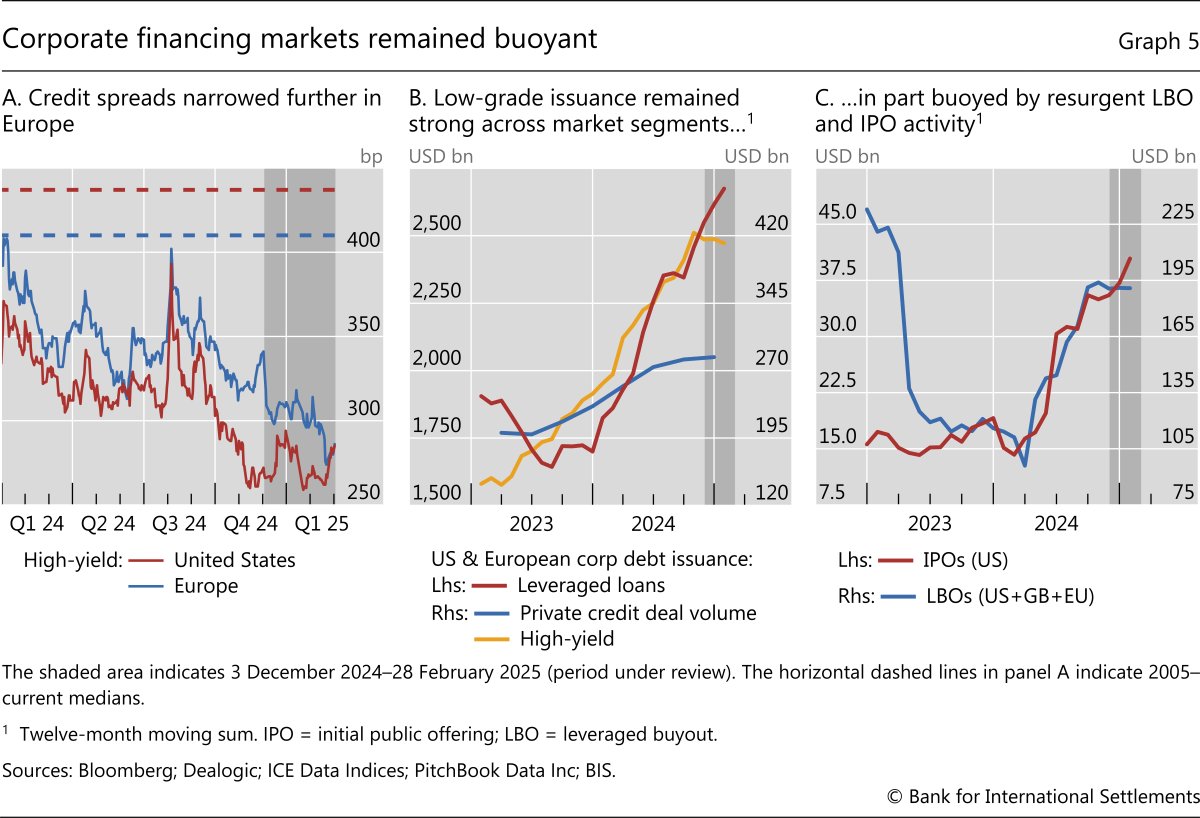

Corporate funding markets remained robust, with issuers taking advantage of the resilient risk sentiment. Credit spreads compressed further across the rating spectrum, particularly for European high-yield bonds, and stayed widely below historical watermarks (Graph 5.A). In this context, issuance remained strong even in the lower-grade segments. Leveraged loan issuance picked up pace (Graph 5.B, red line) amid the continued resurgence of LBO activity (Graph 5.C, blue line). Finally, the long dormant initial public offering (IPO) market extended its 2024 recovery (red line), with a sizeable number of firms brought public and strong first-day performance, particularly during the fourth quarter.

Other corners of private markets also benefited from the positive sentiment. Private credit continued to exhibit strong momentum and closed the year at strength, despite losing some ground to banks' leveraged lending. Venture capital funds saw strong fundraising given the sustained interest of investors in AI bets. The growth investment segment also saw a material improvement, amid a flurry of mergers and acquisitions.

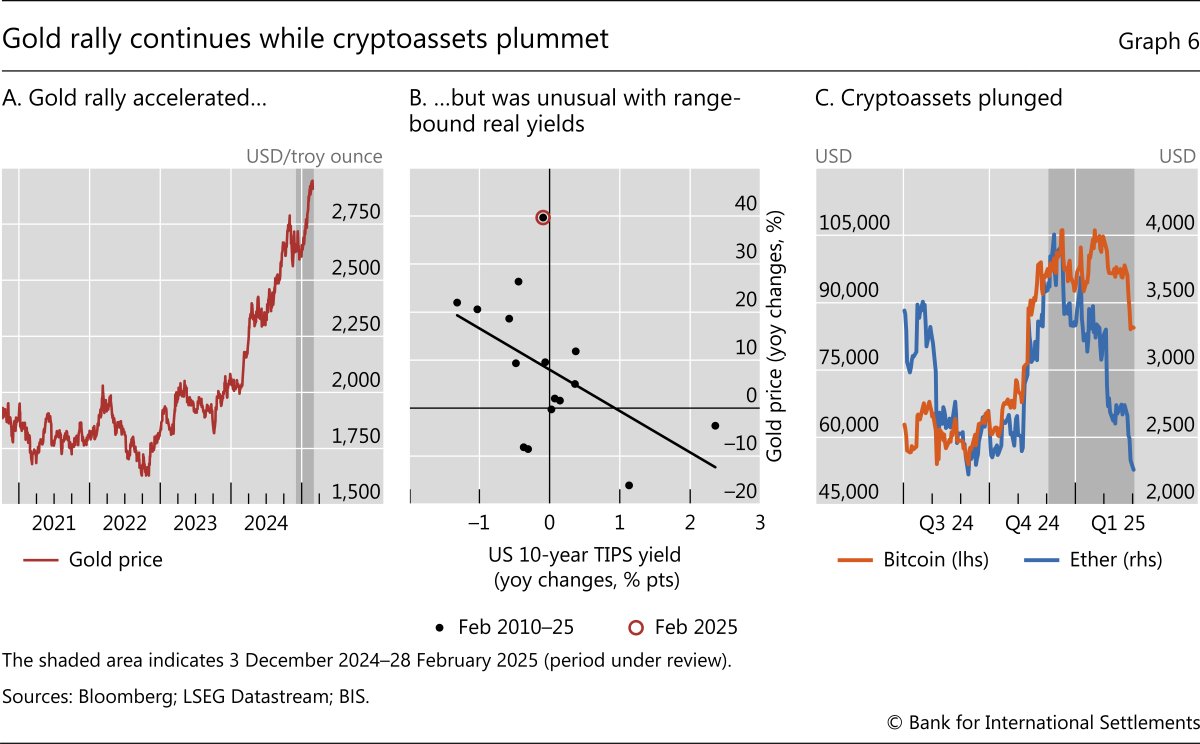

In contrast to the pressures faced by traditional safe havens, the price of gold sustained its strong upward momentum and gained pace during the review period – yet another case of markets being subject to cross-currents. Gold prices rose steadily during the period, irrespective of the wide fluctuations elsewhere (Graph 6.A). The 2024 rally in gold prices was unusual, as it coincided with a stronger US dollar and increasing real yields (Graph 6.B). In the crypto space, bitcoin lost momentum while ether plummeted (Graph 6.C).

Subdued sentiment towards EMEs

Financial conditions in EMEs generally tightened, but to differing degrees. The dollar provided mild relief as its appreciation against EME currencies took a breather. But headwinds gained strength amid generally mediocre macroeconomic conditions, the threat of tariffs and still sluggish growth in the Chinese economy.

Central banks' decisions reflected the diverse domestic conditions and constraints from the Federal Reserve pausing its easing. In Latin America, most central banks cut rates during the review period, as their easing cycle may not be completed yet. Brazil was the exception, hiking rates by 200 basis points in the midst of persistent inflationary pressures. In other parts of the world, notably in Europe and Asia, policy rate cuts were prevalent. In China, benchmark loan prime rates remained stable while the central bank ramped up measures to stabilise the renminbi exchange rate.

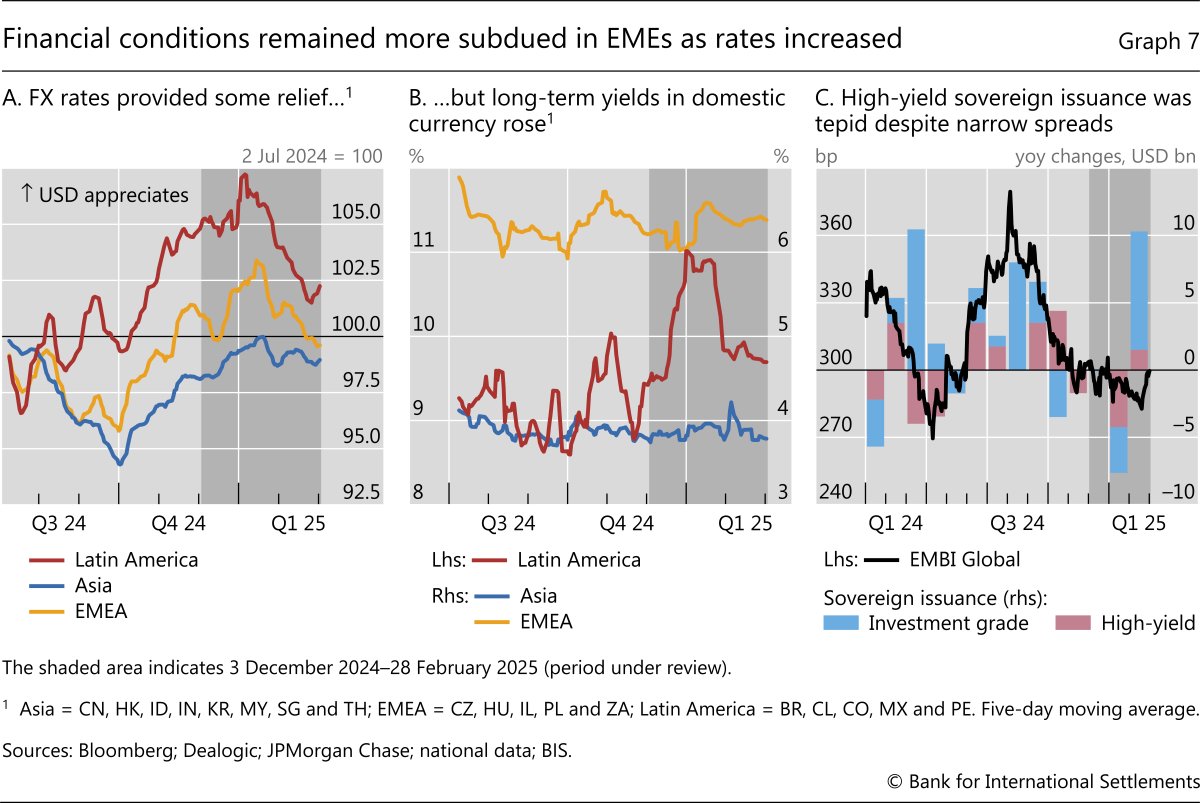

The appreciation of the US dollar stalled during this review period, and several EME currencies appreciated against the greenback. That was particularly the case of Latin American and EMEA (European, Middle Eastern and African) currencies, which largely rebounded from their pronounced Q4 2024 slide amid wide fluctuations (Graph 7.A, red and yellow lines). Asian EME currencies also saw ample swings in their parities, as US trade policy uncertainty mounted, and slightly depreciated over the review period (Graph 7.A, blue line). Carry trade activity, where investors borrow in low-yielding currencies to invest in higher-yielding ones, was likely limited as high volatility made the returns on such trades riskier and less attractive. That said, the conjuncture could quickly change, as evidenced by the August 2024 episode.3

Yields on government bonds in domestic currency generally saw upward pressure, tightening financial conditions. Yields whipsawed in Latin America and EMEA and stayed largely unchanged in Asia. The rise was particularly sharp at the long end of Brazil's term structure, as fiscal concerns took centre stage in investors' view. Other countries in Latin America saw more stable yields, in coincidence with developments in other regions (Graph 7.B).

Issuance of dollar-denominated bonds was mixed despite falling spreads. The easier financial conditions of AE credit markets reflected more clearly on the spreads of dollar-denominated bonds, which compressed by about 20 basis points (Graph 7.C). Despite that compression, sovereign issuance remained generally circumspect, especially in the high-yield segment, although it gained some traction in February within the investment grade sovereign segment.

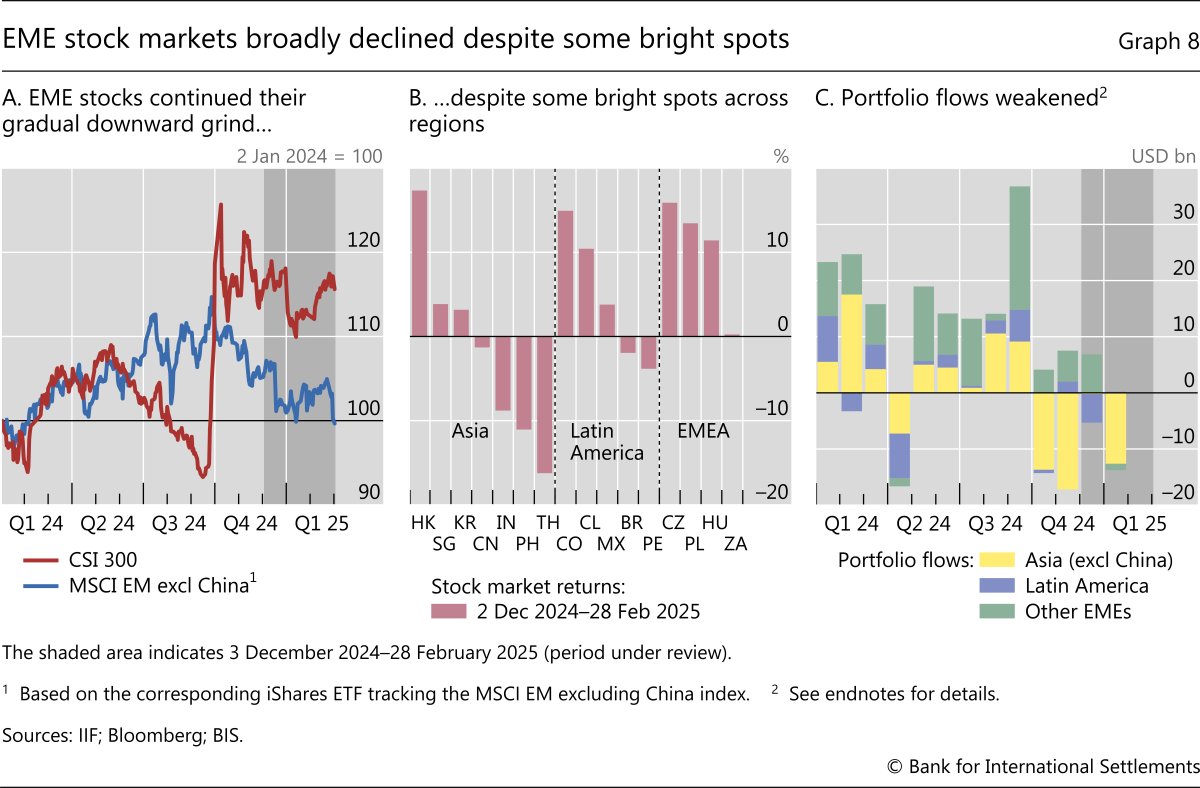

EME stock markets trended downwards on average, adding to the tightening pressure on financial conditions. Chinese equity markets saw a rebound in February after months-long weakness, and ended the period flat (Graph 8.A, red line) on the back of improving sentiment and optimism related to the outlook for AI. This sudden awakening of the continental market was also reflected in Hong Kong SAR equities, whose valuations soared. Additionally, there were bright spots in some small Latin American markets and in EMEA, the latter seemingly pulled by the momentum of the major European exchanges (Graph 8.B). Moreover, India's IPO market continued its strong performance in the fourth quarter, having contributed a sizeable volume share to the global IPO market in 2024.

Overall, however, sentiment towards EMEs remained downcast. With attractive yields on safe debt of AEs, foreign investors in EME debt securities extended the caution that characterised the last quarter of 2024. Portfolio flows turned negative for emerging Asia, in line with the lacklustre stock performance and lower yields (Graph 8.C). Flows into other EMEs also weakened, reflecting the overall anaemic sentiment.

Endnotes

Graph 8.C: Emerging Asia = ID, IN, KR, LK, MN, MY, PH, PK, TH, TW and VN; Latin America = BR, CL, CO, and MX; other EMEs = BG, CZ, EE, GH, HU, KE, LB, LT, LV, MK, PL, QA, RO, RS, RU, SA, SI, TR, UA and ZA.

1 The period under review extends from 3 December 2024 through 28 February 2025.

2 It is noteworthy that these spreads are negative since private financial instruments typically carry higher risks (eg credit risk) such that corresponding yields should in principle be higher than those of government bonds. The uncommon sight of government bonds yielding more than private sector instruments suggests that investors and intermediaries are demanding higher compensation to absorb government debt supply, although to different degrees across countries. For a discussion of the drivers of interest rate swap spreads, see M Aquilina, A Schrimpf, V Sushko and D Xia , "Negative interest rate swap spreads signal pressure in government debt absorption", BIS Quarterly Review, December 2024.

3 See "Carry off, carry on", BIS Quarterly Review, September 2024.