Statistical release: BIS international banking statistics and global liquidity indicators at end-September 2024

Key takeaways

- During the third quarter of 2024, banks' cross-border claims expanded by $629 billion, up 3.4% year on year.

- The expansion in claims was primarily driven by cross-border bank credit (ie loans and holdings of debt securities) to non-bank financial institutions (NBFIs) in advanced economies.

- Cross-border bank credit to emerging market and developing economies expanded, notwithstanding a contraction vis-à-vis China.

- The BIS global liquidity indicators reveal that the ongoing weakness in dollar and euro credit to emerging Asia dates back to the respective starting points of the post-Covid Federal Reserve and ECB tightening cycles.

Global cross-border bank credit expands

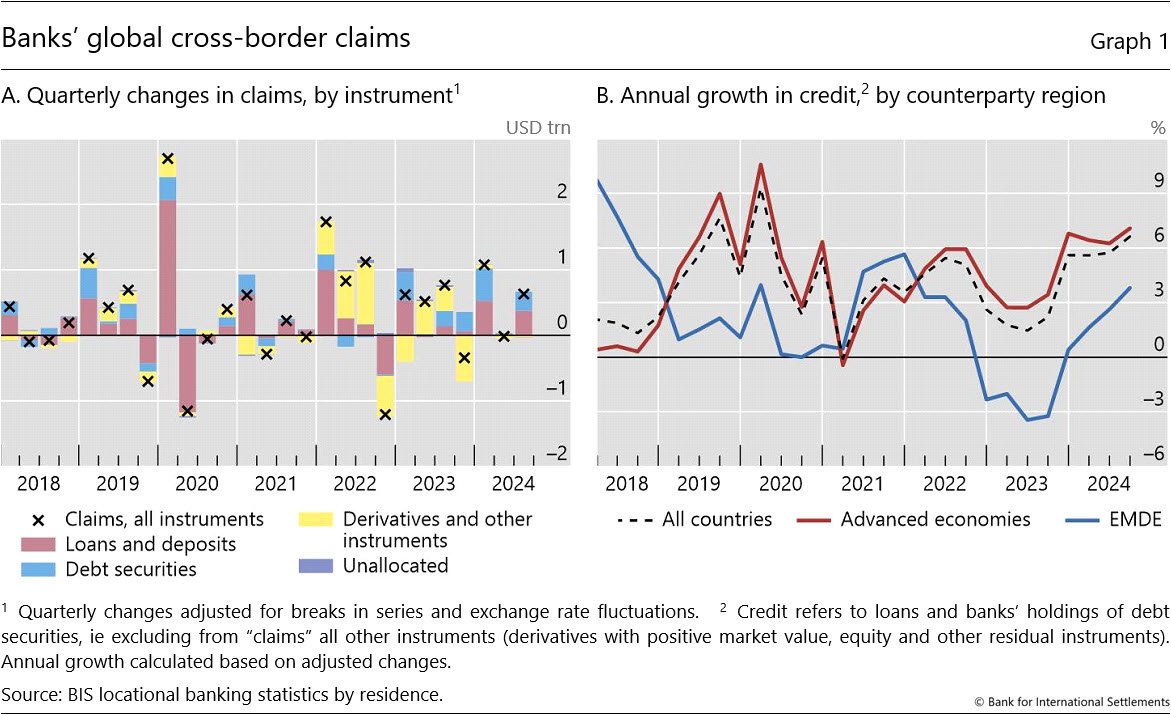

The BIS locational banking statistics (LBS) reveal that banks' global cross-border claims rose by $629 billion on an exchange rate- and break-adjusted basis in Q3 2024 (Graph 1.A), This pushed the outstanding stock to $41 trillion, up 3.4% from a year earlier.

The expansion in claims during Q3 2024 was exclusively driven by cross-border bank credit (ie loans and holdings of debt securities but excluding derivatives and other claims).1 Most of the expansion ($613 billion) went to borrowers in advanced economies (AEs), driving the annual growth rate to 7.1%, the highest since Q1 2020 (Graph 1.B). Concurrently, cross-border credit to emerging market and developing economy (EMDE) borrowers rose by $35 billion (+3.8% year on year (yoy)).

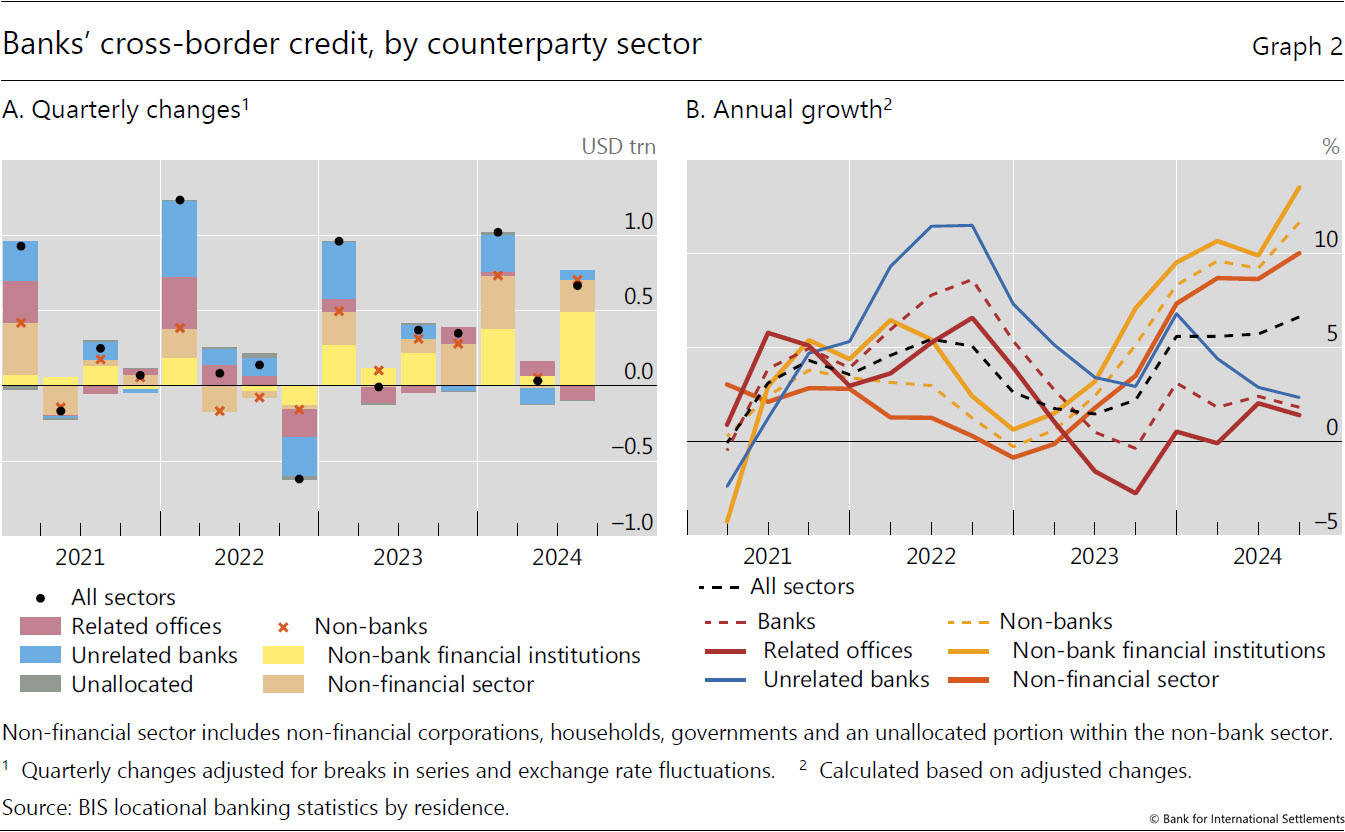

The expansion in cross-border credit during Q3 2024 was driven by a $704 billion rise in lending to the non-bank sector (Graph 2.A, crosses). This extended a trend that originated at the beginning of 2023 and pushed the annual growth of the series to 12% (Graph 2.B, dashed yellow line). Cross-border credit to non-bank financial institutions (NBFIs) surged by $495 billion, reaching an annual growth rate of 14%, the highest since Q3 2019. Cross-border credit to the non-financial sector (NFS) also grew strongly, expanding by $209 billion during the quarter (+11% yoy).

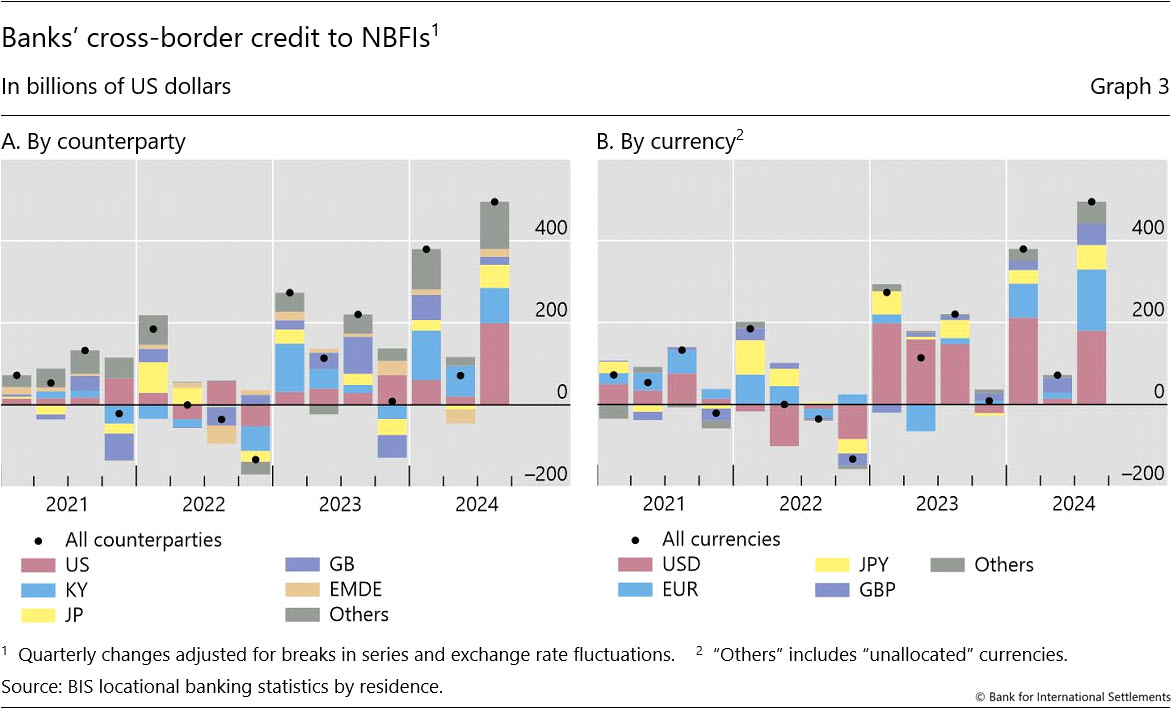

The growth in cross-border credit to NBFIs was quite broad-based across borrowing countries (Graph 3.A) and denomination currencies (Graph 3.B). The expansions in cross-border credit to NBFIs in the United States ($199 billion) and Japan ($56 billion) were primarily driven by credit denominated in the respective borrowers' domestic currencies. Dollar credit to NBFIs in the United States grew by $140 billion, while yen credit to the same sector in Japan went up by $55 billion. The $87 billion expansion vis-à-vis NBFIs in the Cayman Islands was driven by increases in euro (+$35 billion), sterling (+$19 billion), US dollar (+$11 billion) and yen (+$6 billion) credit.

By contrast, cross-border interbank lending remained sluggish, expanding at a modest annual pace of 1.8% (Graph 2.B, dashed red line). Credit to unrelated banks increased by $61 billion (+2.4% yoy). Meanwhile, inter-office credit contracted by $99 billion, which brought down its annual growth rate to 1.4%.

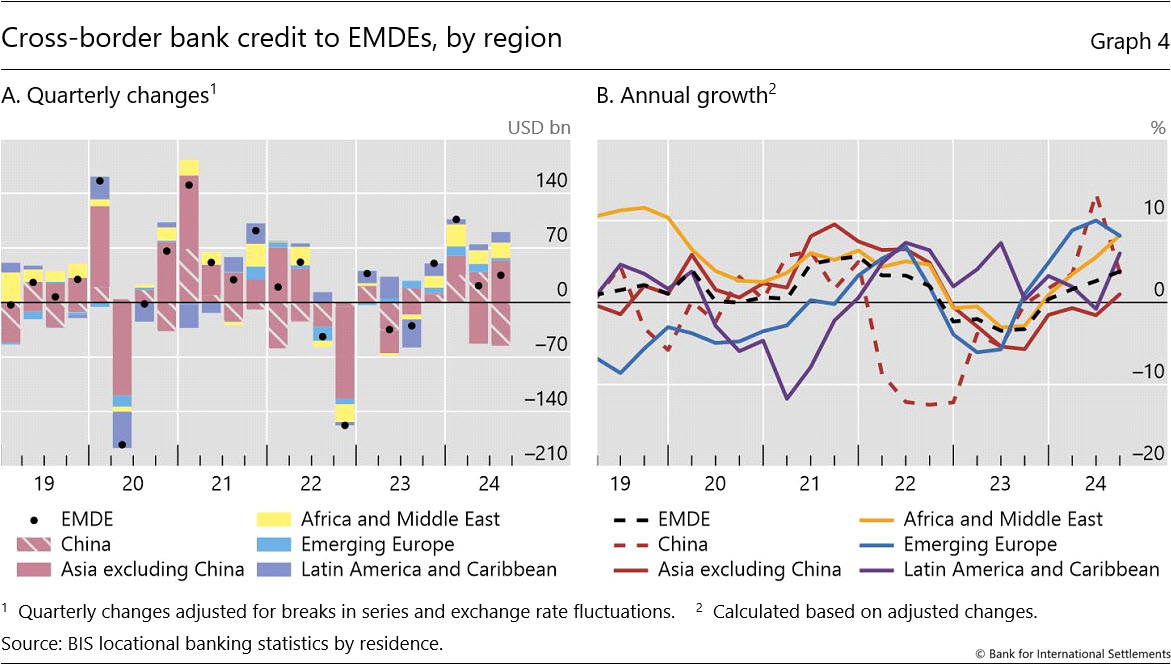

Cross-border credit to EMDEs rose for the fourth consecutive quarter in Q3 2024 (Graph 4.A, black dots). The $35 billion expansion in Q3 2024 brought the annual growth rate of the series up to 3.8% (Graph 4.B, dashed black line).

In contrast to the overall expansion, cross-border lending to China contracted by $55 billion. Credit to the rest of the emerging Asia-Pacific region grew by $54 billion, which brought its annual growth rate back into positive territory for the first time since Q3 2022 (Graph 4.B, red line).

Cross-border lending to all other EMDE regions also expanded. Credit to Africa and the Middle East and Latin America and the Caribbean rose by $20 billion and $13 billion, respectively, while that to emerging Europe inched up by $3 billion.

Global liquidity indicators at end-September 2024

The BIS global liquidity indicators (GLIs) track total credit to non-bank borrowers, covering both loans extended by banks and funding from international bond markets.2 The latter is captured through the net issuance (gross issuance less redemptions) of international debt securities (IDS). The focus is on foreign currency credit denominated in the three major reserve currencies (US dollar, euro and Japanese yen) to non-residents, ie borrowers outside the respective currency areas.

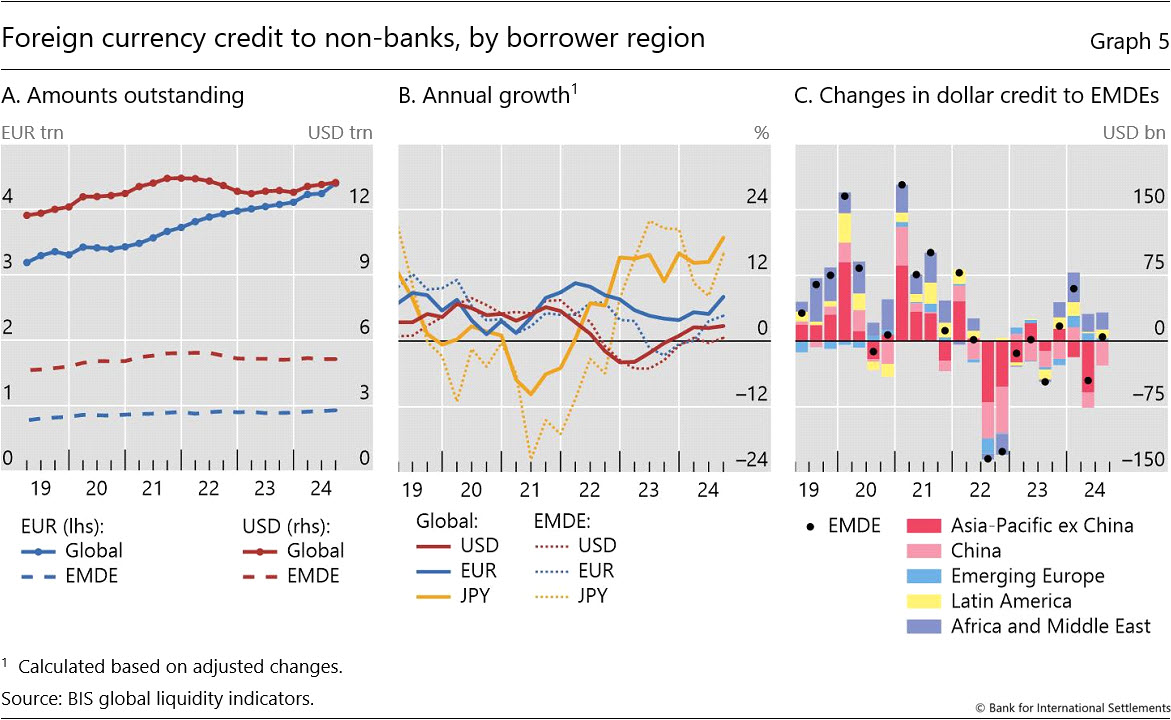

Global foreign currency credit denominated in all three major currencies saw modest increases in Q3 2024. The $89 billion rise in dollar credit to non-banks outside the United States took its outstanding stock to $13.2 trillion (Graph 5.A, solid red line) and its annual growth rate to 2.7% (Graph 5.B, solid red line). Euro credit to non-banks outside the euro area expanded by €157 billion (8.1% yoy) and reached €4.4 trillion ($4.9 trillion) (Graphs 5.A and 5.B, solid blue lines). Yen credit to non-banks outside Japan rose by ¥263 billion in Q3 2024. This brought its outstanding stock to ¥64.7 trillion ($453 billion) and its annual growth rate to 19% (Graph 5.B, solid yellow line).

Foreign currency credit to EMDEs also saw modest increases for the three major currencies in Q3 2024 (Graph 5.A, dashed lines). Dollar credit to EMDEs rose by $5 billion (0.6% yoy), notwithstanding a contraction of $28 billion vis-à-vis China (Graph 5.C). Euro credit to EMDEs also increased slightly (€12 billion), primarily driven by Africa and the Middle East and emerging Europe. Meanwhile, yen credit rose by ¥415 billion ($3 billion), driven by emerging Asia-Pacific and Latin America and the Caribbean.

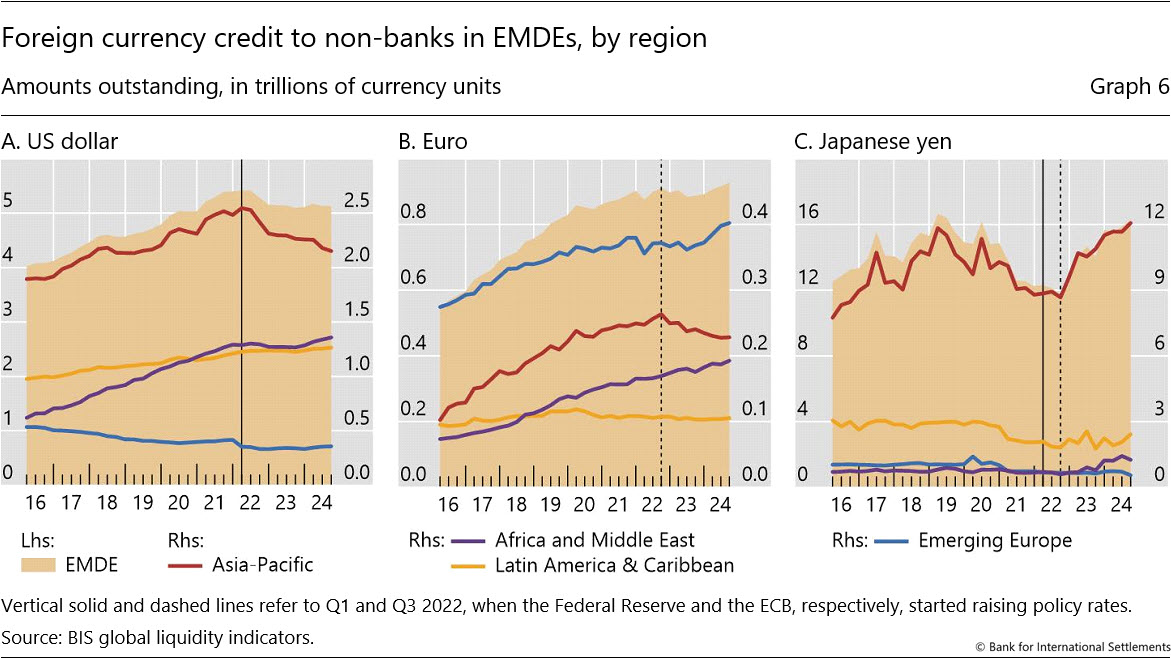

Taking a longer perspective, the ongoing trends in foreign currency credit to emerging Asia-Pacific date back to the starting points of the post-Covid Fed and ECB tightening cycles. Dollar credit to the region peaked in Q1 2022, when the Fed embarked on its latest tightening cycle. Since then, it has declined by almost $400 billion, or 15% (Graph 6.A, red line). Roughly half of this contraction was driven by dollar credit to China. Similarly, euro credit to emerging Asia-Pacific peaked in Q3 2022, when the ECB started raising its policy rate, and has contracted by €35 billion (or 13%) since then (Graph 6.B, red line). By contrast, yen credit to the region expanded by ¥3.2 trillion (or 36%) since Q1 2022 (Graph 6.C, red line).

In contrast to emerging Asia, the current trends in foreign currency credit to the other EMDE regions started long before the Covid pandemic. Dollar and euro credit to Africa and the Middle East have been rising steadily for almost a decade (Graphs 6.A and 6.B, purple lines). The notable divergence between (rising) euro and (falling) dollar credit to emerging Europe started in 2016 (Graphs 6.A and 6.B, blue lines). In the meantime, euro credit to Latin America has remained relatively flat, while dollar credit to the region has been on a modest, but steady rising path (Graphs 6.A and 6.B, yellow lines).

1 In the BIS LBS, bank claims comprise: (i) loans and deposits; (ii) holdings of debt securities; and (iii) derivatives with a positive market value and other residual instruments (combined). Credit is defined as the sum of (i) and (ii).

2 The GLIs cover total foreign currency credit denominated in US dollars, euros or Japanese yen, which includes loans from banks plus outstanding international bonds. This is broader than "bank credit" covered in previous sections, which captures banks' loans and their holdings of debt securities.