BIS residential property price statistics, Q2 2024

Key takeaways

- Global house prices continued to decline in the second quarter of 2024, with a 1.4% year-on-year (yoy) decrease in aggregate and real terms, driven by sharp decreases in large emerging market economies (EMEs) in Asia.

- Median house prices increased slightly, as more than 60% of jurisdictions globally saw an increase in real house prices.

- Real house prices increased moderately in advanced economies (AEs) for the first time since Q3 2022 (+0.2%), while they continued to decline (–2.6%) in EMEs.

- Differences persist across major economies. In AEs, real house prices fell in Europe, while they increased in non-European countries. In EMEs, prices fell in Asia but rose in all other regions.

- From a longer-term perspective, real global house prices remain 21% above their average level observed in the aftermath of the 2007–09 Great Financial Crisis (GFC).

Summary of latest developments

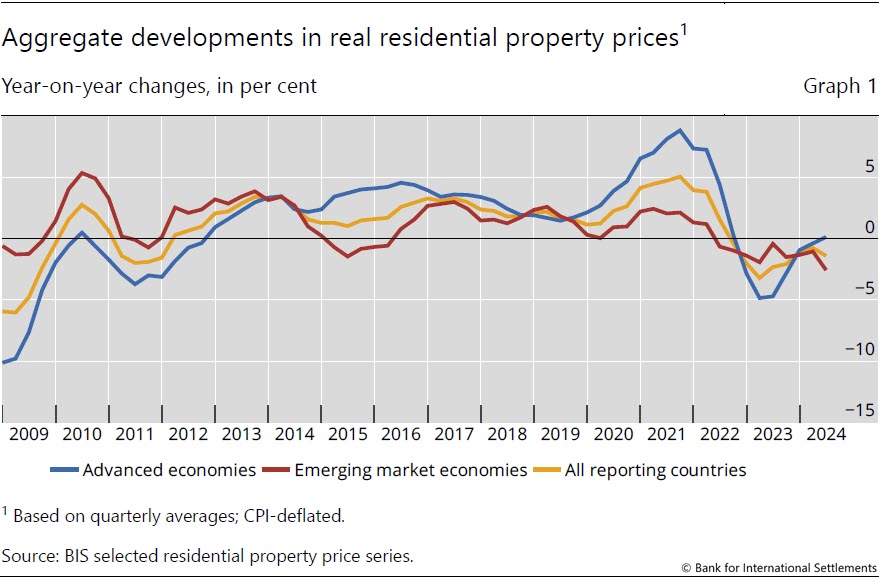

In the second quarter of 2024, global house prices deflated by consumer prices declined by 1.4% yoy, compared with –0.8% in the first quarter.1 This decline was despite the continuous moderate increase registered in nominal terms (+2.5%).

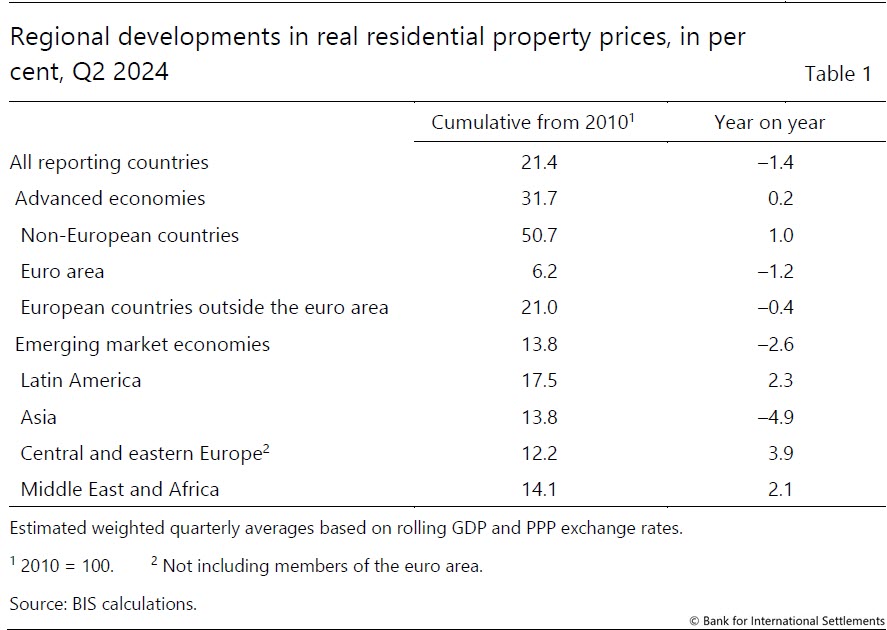

Developments diverged further between AEs and EMEs in Q2 2024. Real house prices increased in AEs by 0.2% yoy for the first time since Q3 2022, following a prolonged period of decline. In contrast, prices decreased by 2.6% yoy in EMEs, compared with –1.0% in Q1 2024, continuing the downward trend observed since Q2 2022 (Graph 1). The fall in EMEs was mainly caused by the decline observed in Asia (–4.9%), which was only partially offset by increases in central and eastern Europe (+3.9%), Latin America (+2.3%) and the Middle East and Africa (+2.1%) (Table 1).

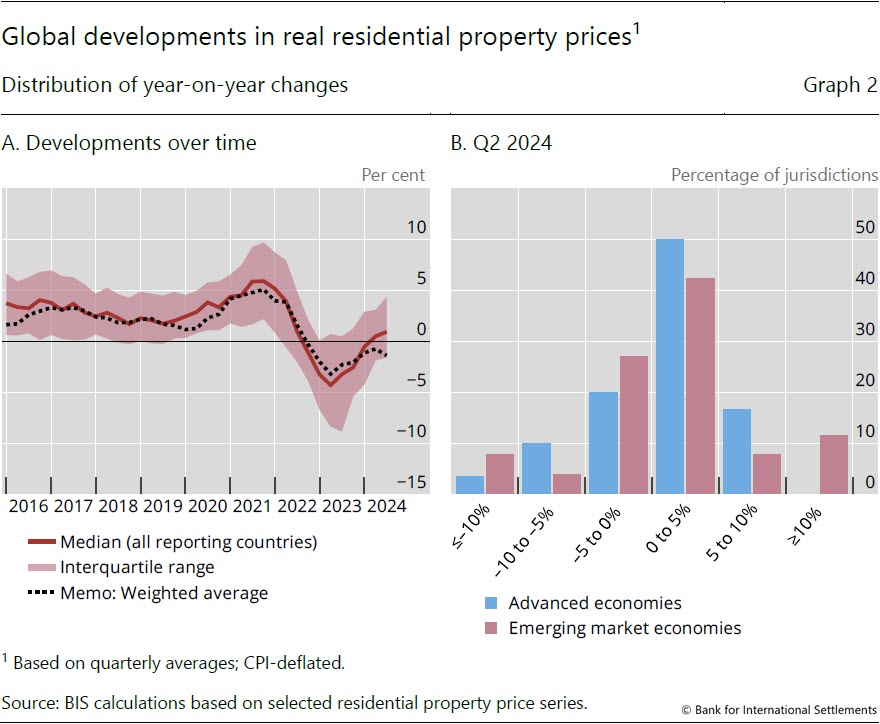

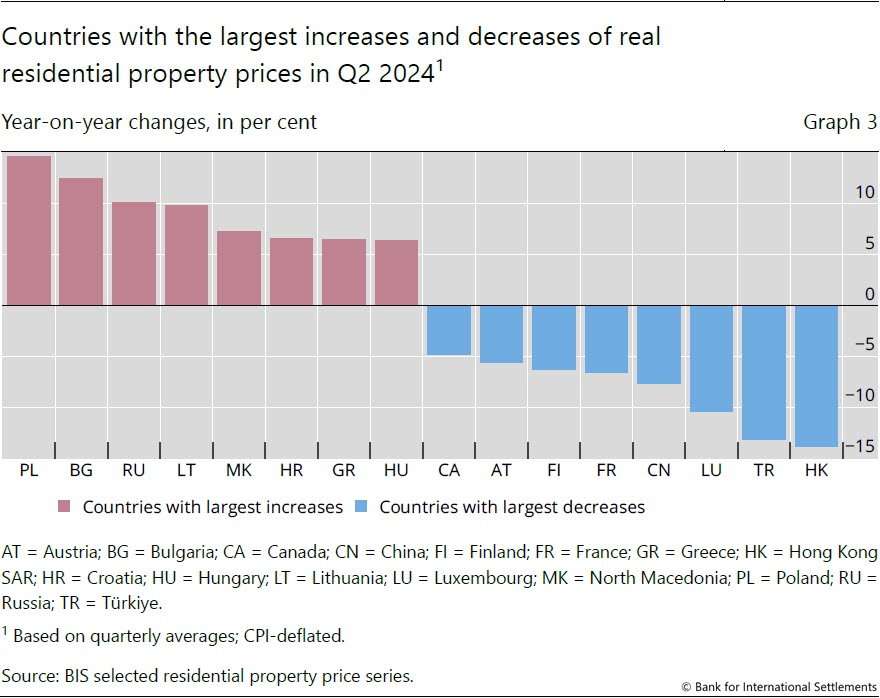

Country-level data reveal that more than 60% of all analysed jurisdictions in both AEs and EMEs experienced an increase in real house prices in Q2 2024, pushing up the median growth to close to 1% (Graph 2.A). This reflects the fact that the continuous decline in global real house prices has been primarily driven by a few major jurisdictions, particularly China (–7.6%) and to a lesser extent India (–1.5%).2 Graph 3 provides a more granular overview of the countries which recorded the largest increases and decreases of real residential property prices in Q2 2024. It shows that prices fell the most in Hong Kong SAR, Türkiye and Luxembourg. In contrast, they rose markedly in Poland and Bulgaria.

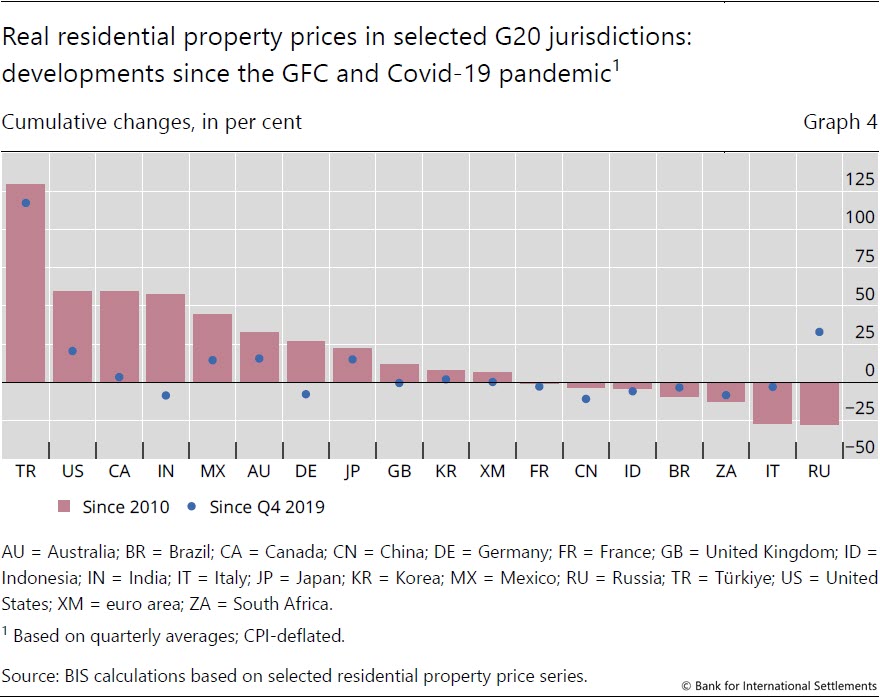

In aggregate, global real residential prices are above their levels before the Covid-19 pandemic (by 4%). Among the G20 economies, and compared with Q4 2019, they have increased by 117% in Türkiye but have declined by 11% in China, 9% in India and 8% in South Africa and Germany (Graph 4).

From a longer-term perspective, real global house prices exceed their post-GFC average by 21% in aggregate for all analysed jurisdictions (32% for AEs and 14% for EMEs) (Table 1). Among G20 economies, they have more than doubled since 2010 in Türkiye and risen by more than 50% in the United States, Canada and India. But they remain below their post-GFC levels in 40% of the jurisdictions (Graph 4).

Advanced economies

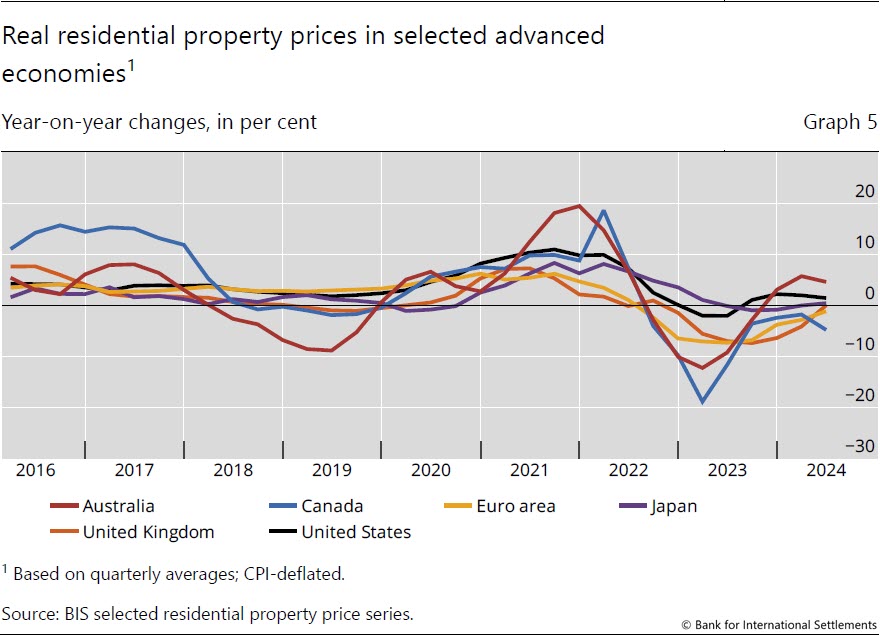

In aggregate for AEs, real residential property prices increased by 0.2% yoy in Q2 2024, the first growth observed since Q3 2022. Among major economies, real prices were up by 4.6% in Australia and 1.4% in the United States and were stable in Japan and the United Kingdom. They continued to fall in Canada (–4.8%) and, to a lesser extent, the euro area (–1.2%) (Graph 5).

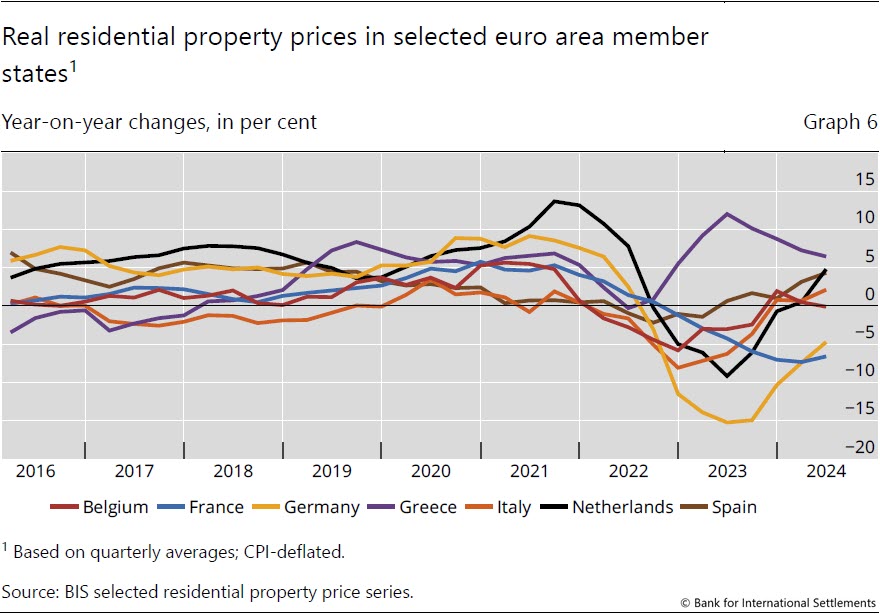

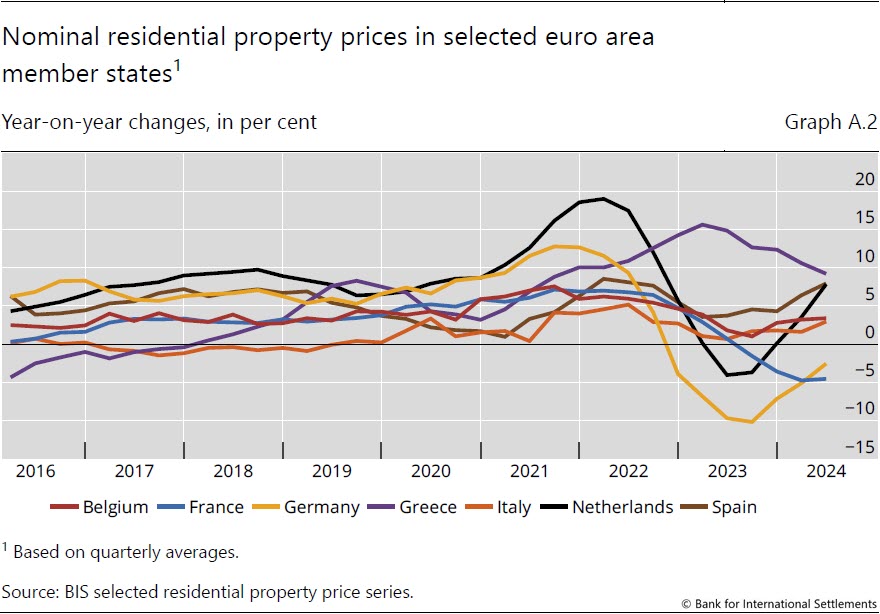

Within the euro area, real house prices continued to show significant variations among member states in Q2 2024. They increased by 6.5% in Greece, 4.8% in the Netherlands and 4.3% in Spain. The increase was more moderate in Italy (+2.1%), while prices remained stable in Belgium (–0.1%). In contrast, they declined in Germany (–4.7%) and even more in France (–6.6%) (Graph 6).

Emerging market economies

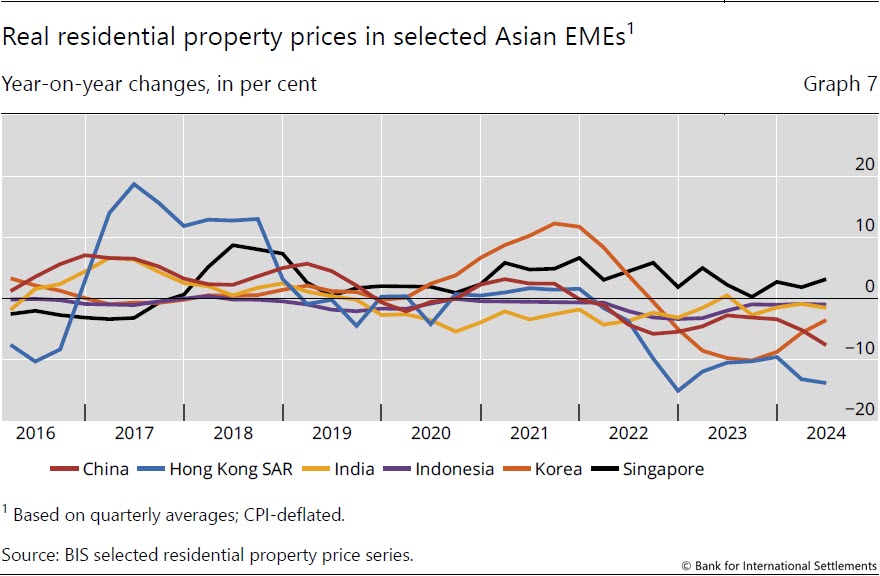

Real residential property prices declined by 2.6% yoy in EMEs during the first quarter of 2024 (compared with –1.0% in Q1 2024), driven by the pronounced fall observed in Asia. In contrast, prices increased in all other regions.

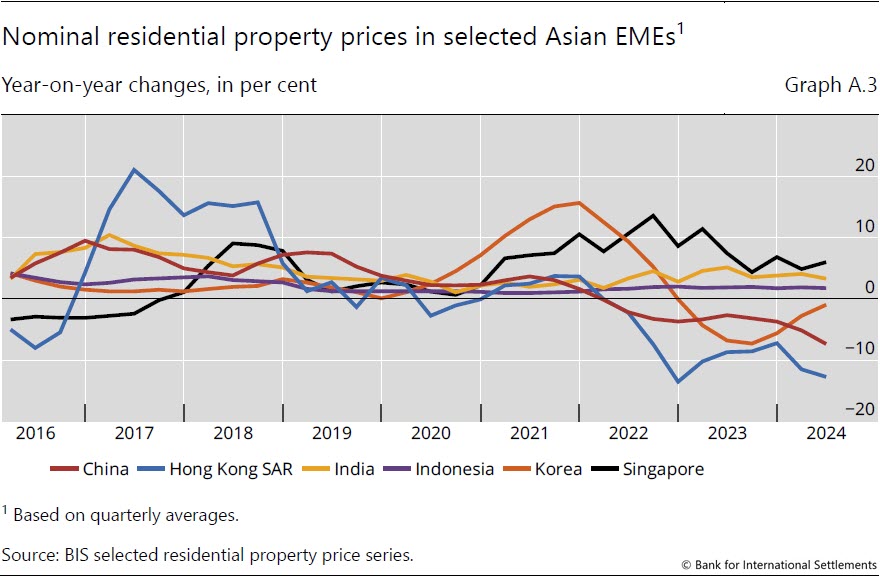

Prices fell by 4.9% on average in Asian economies, with declines of 13.8% in Hong Kong SAR, 7.6% in China, 3.5% in Korea, 1.5% in India and 1% in Indonesia. In contrast, prices increased by 3% in Singapore (Graph 7).

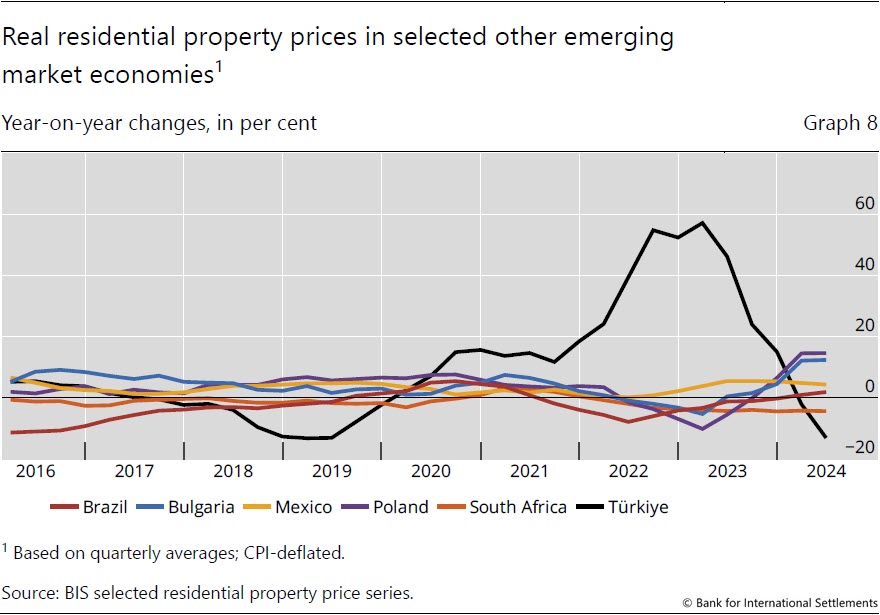

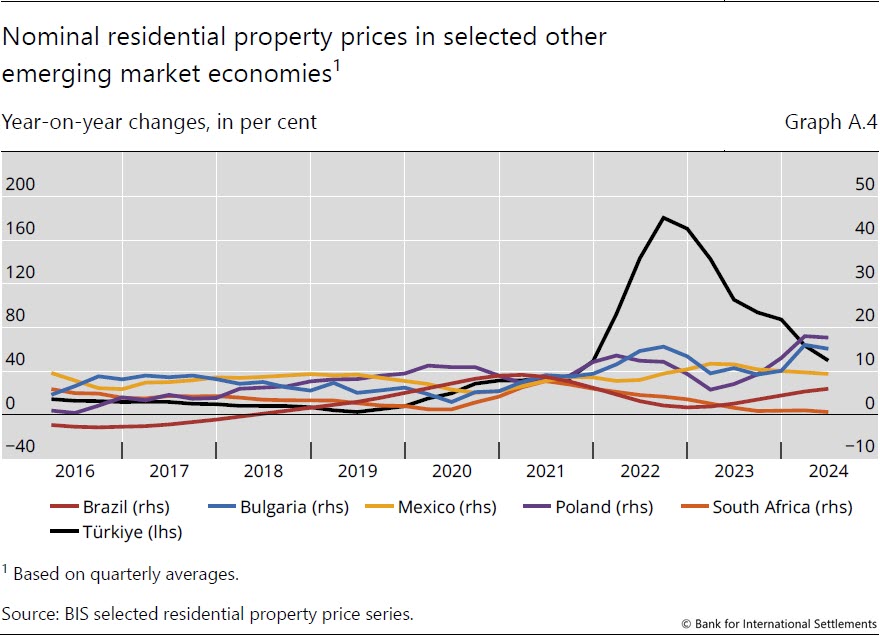

Real prices rose by 2.3% in Latin America, mainly driven by a continued price increase in Mexico (+4.4%) and Brazil (+1.9%). In central and eastern European countries, real prices grew by 3.9% in aggregate, with double-digit growth in Poland (+14.7%) and Bulgaria (+12.4%). Prices continued to decline in Türkiye (–13.1%) and South Africa (–4.3%) (Graph 8).

Annex: Nominal house price developments

1 Real residential property prices refer to nominal residential property price indicators deflated by the consumer price index. Global figures are weighted aggregates of selected AEs (Australia, Canada, Denmark, the euro area, Iceland, Japan, New Zealand, Norway, Sweden, Switzerland, the United Kingdom and the United States) and EMEs (Brazil, Bulgaria, Chile, China, Colombia, Czechia, Hong Kong SAR, Hungary, India, Indonesia, Israel, Korea, Malaysia, Mexico, Morocco, North Macedonia, Peru, the Philippines, Poland, Romania, Russia, Singapore, South Africa, Thailand, Türkiye and the United Arab Emirates), based on PPP exchange rates. Regional aggregates have been available since 2007.

2 As regional aggregate developments are driven mainly by changes in major economies, they can mask the detailed country-level features presented in the histogram.

Indeed, looking more closely at the distribution, around 70% of all jurisdictions saw moderate price changes in Q2 2024, between –5 and +5% yoy (Graph 2.B).