Figures accompanying the speech

Thank you, Jacky. I am happy to be here in Adelaide and appreciate the opportunity to speak with all of you.Considering the significant developments in the global economy over the past few years, now is an appropriate time to reflect on the economic reverberations the COVID-19 shock caused around the world. Examining the common inflation experiences and monetary policy challenges across several countries, including Australia and the United States, is a helpful exercise for policymakers and economists alike. Today, I will first talk about how monetary policymakers responded in similar fashion to the COVID-19 pandemic and, later, to high inflation during the recovery. I will discuss common features of the recent inflation experience across countries and the importance of global shocks. With disinflation in train across most countries, I will consider what we can learn from past cycles of monetary easing. I will finish with a discussion of how the use of alternative scenarios could help monetary policymakers communicate how they might respond to a range of possible economic outcomes.

Common Monetary Policy Response to the Pandemic

In the spring of 2020, economies around the world shut down or sharply limited business activity, especially for in-person services, including dining out and traveling. Governments introduced extraordinary fiscal support aimed at alleviating the socioeconomic effects of the pandemic. And, to prevent sharp financial and economic deterioration, most central banks responded aggressively by lowering policy rates, ramping up asset purchases, and taking other actions to support the flow of credit to households and businesses. Those efforts were sustained throughout 2020 and much of 2021, as the initial turmoil in financial markets subsided but the health situation remained uncertain.

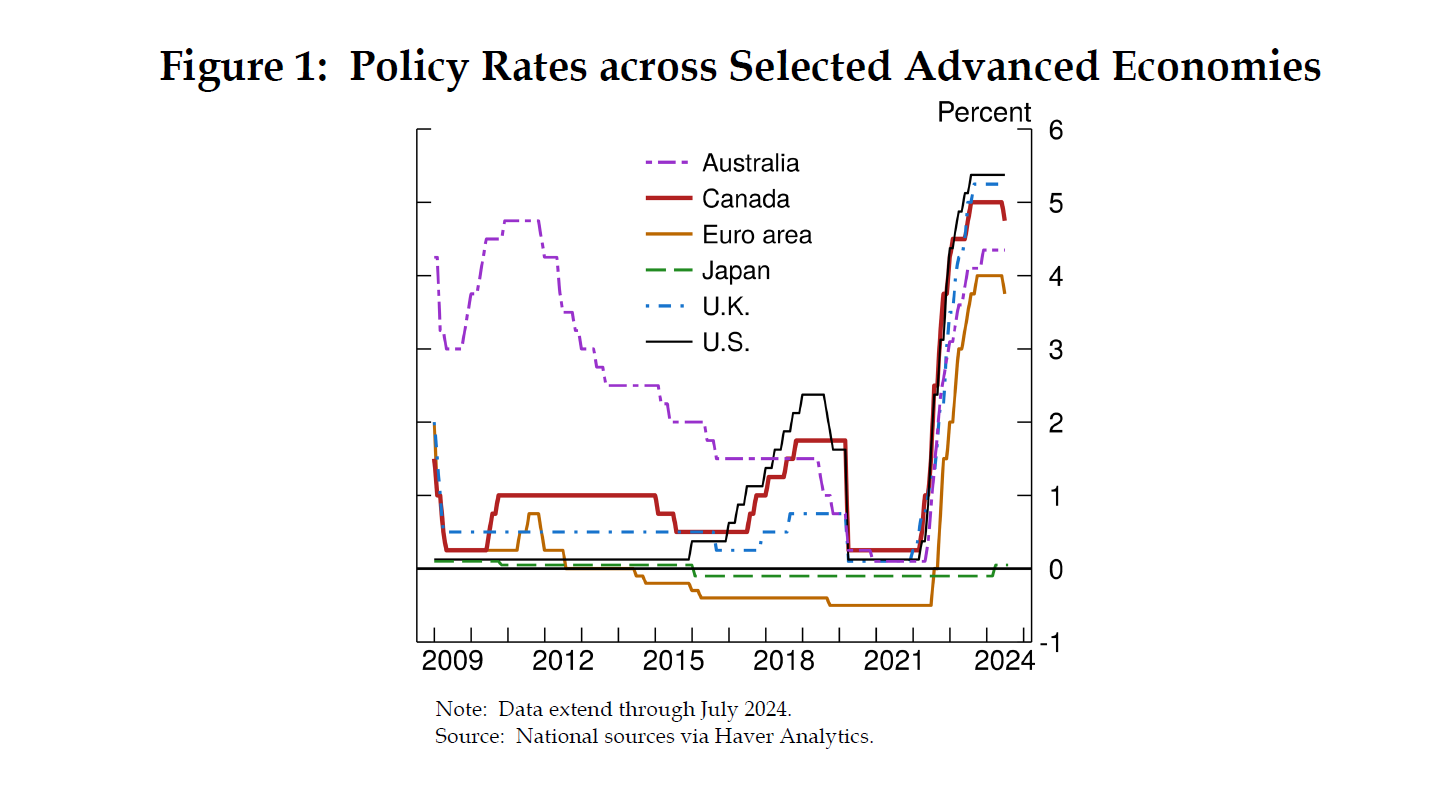

Advanced economy central banks that had positive policy rates before the pandemic, including the Fed and the central banks of Australia, Canada, and the United Kingdom, cut these rates to near zero, as shown in figure 1. Central banks that entered the pandemic with policy rates already at zero, such as Sweden, or negative-including the euro area, Japan, and Switzerland-left their rates unchanged. Meanwhile, almost all emerging market economy (EME) central banks cut their policy rates. Although central banks acted quickly to reduce rates, policymakers cited a few reasons to refrain from deeper cuts: Among EME policymakers, concerns were expressed that further lowering rates risked exacerbating capital outflows, while some advanced economy central banks commented that further rate cuts, particularly in negative territory, could harm banks' financial health or would provide little additional monetary stimulus.

{kind=link}