Philip N Jefferson: US economic outlook and monetary policy transmission

Speech by Mr Philip N Jefferson, Member of the Board of Governors of the Federal Reserve System, at the "Beyond the Business Cycle: Adapting to a New Global Paradigm" 65th Annual Meeting of the National Association for Business Economics, Dallas, Texas, 9 October 2023.

The views expressed in this speech are those of the speaker and not the view of the BIS.

Introduction

Thank you for inviting me to join this conference and for the kind introduction. It is a pleasure to be here.

Before I begin, let me remind you that the views I will express today are my own and are not necessarily those of my colleagues in the Federal Reserve System.

I will take this opportunity to share with you my outlook on the U.S. economy. I will also discuss risks facing the economy. Then, I will turn to the transmission of monetary policy, including some recent evidence on a source of lagged effects of policy. Finally, I will discuss considerations for monetary policy that follow from efforts to manage risks given the lagged effects of monetary policy. These considerations include the need to proceed carefully as the risks of tightening monetary policy too much relative to those of not tightening enough move closer into balance. With that, let me turn to my outlook for the U.S. economy.

The Inflation Outlook

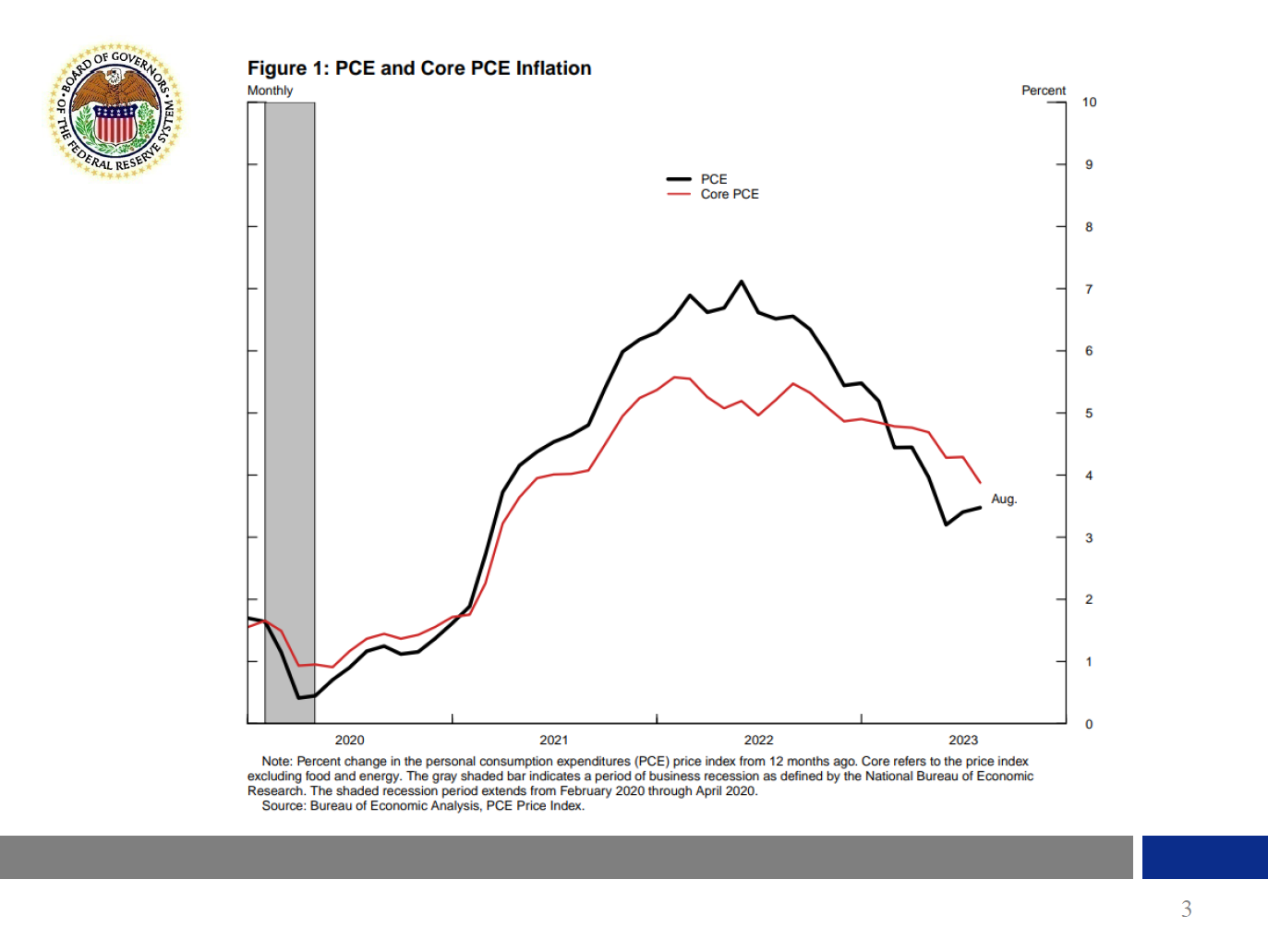

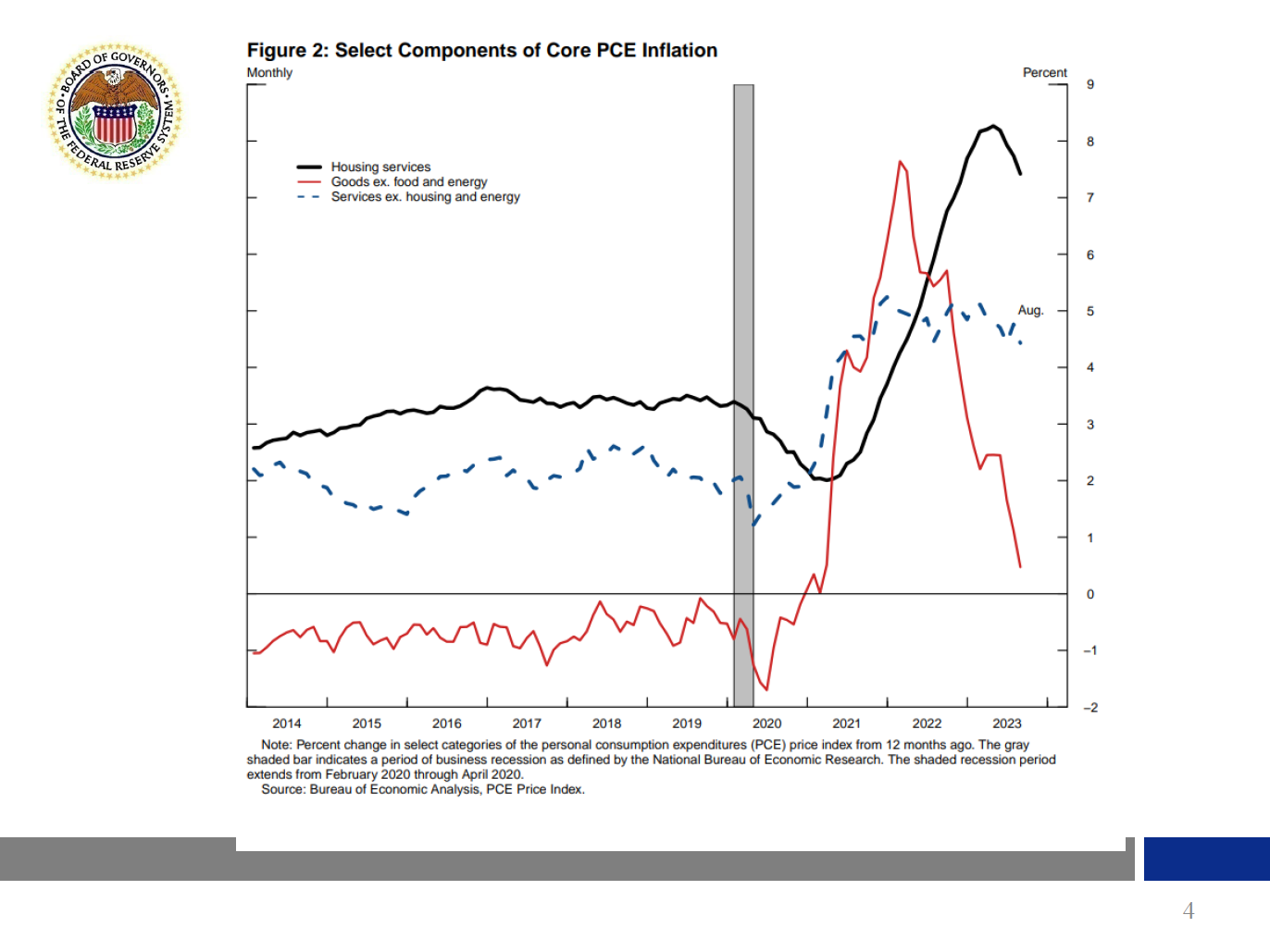

Even though recent inflation data have been encouraging, inflation remains too high. Over the 12 months ending in August, total Personal Consumption Expenditures (PCE) prices rose 3.5 percent, the black line in figure 1. Excluding the volatile food and energy categories, core PCE prices rose 3.9 percent, the red line. To better understand core inflation trends, I find it useful to look at three large categories that together make up the core PCE price index, because what has been causing inflation in each of these sectors is somewhat different. The first category, core goods inflation, the red line in figure 2, has slowed strikingly, as supply chain–related price pressures continue to ease. The second category, housing services price inflation, the black line, has clearly stepped down, as was anticipated given the previous slowing of increases in rents for new tenants. In contrast, price increases for the third category, core nonhousing services, the blue line, have yet to show a significant slowdown. Since this segment accounts for more than 50 percent of the overall core PCE index, we will need to see further slowing in this area to meet our inflation objective. Nevertheless, I believe that core PCE prices will moderate further as the labor market comes into better balance.

{kind=link}

{kind=link}