Bank CP rates amid asymmetric funding-liquidity conditions across currencies

Box extracted from Overview chapter "Resilient risk-taking in financial markets"

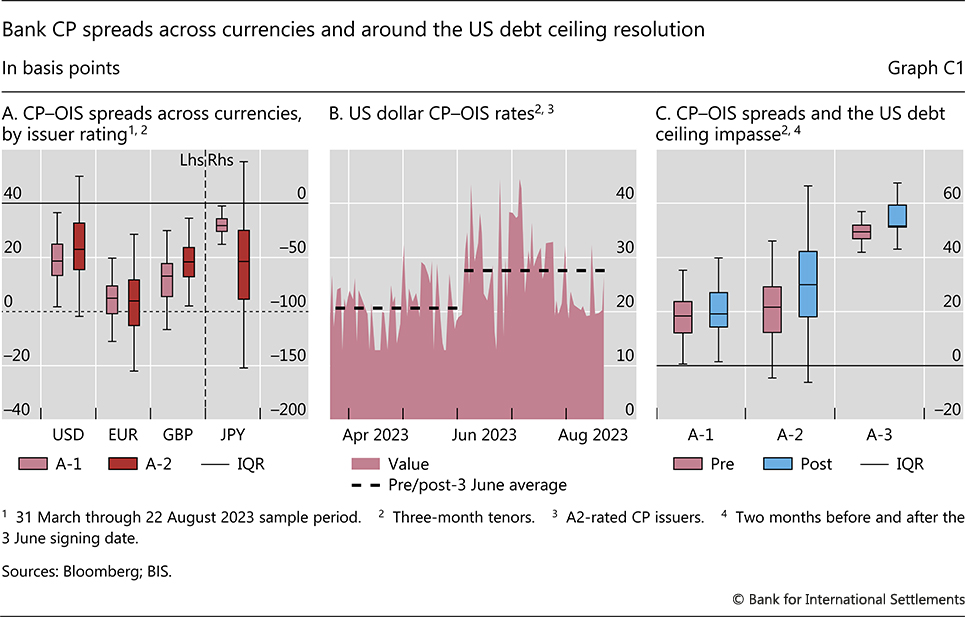

Commercial paper (CP) markets constitute an important source of unsecured funding for banks (Aquilina et al (2023, in this issue)).*  Bank CPs are short-term (one- and three-month) and are issued at rates that track other money market rates fairly closely, albeit with a time-varying spread relative to the (nearly) risk-free benchmarks, such as overnight index swap (OIS) rates. A wider (positive) CP-OIS spread indicates tighter funding conditions for banks, reflecting liquidity risk and credit risk premia.

Bank CPs are short-term (one- and three-month) and are issued at rates that track other money market rates fairly closely, albeit with a time-varying spread relative to the (nearly) risk-free benchmarks, such as overnight index swap (OIS) rates. A wider (positive) CP-OIS spread indicates tighter funding conditions for banks, reflecting liquidity risk and credit risk premia.

This box studies bank CP spreads across major currencies. It highlights apparent anomalies in CP market pricing that probably stem from abundant liquidity. It also documents how US dollar CP spreads responded to the resolution of the US debt ceiling impasse in early June. The data comprise quotes by CP dealers on the Bloomberg trading platform, posted during the liquid trading hours in Europe and the US: two snapshots per day, from 31 March to 22 August 2023. They also cover issuer identity, tenor, currency denomination and credit rating.

In some currencies, the CP-OIS spread suggests anomalies as regards the compensation that investors demand for liquidity and/or credit risk. While CP-OIS spreads are positive in the US dollar and the British pound, they are approximately zero in the euro and negative in the Japanese yen (Graph C1.A). In the first two currencies, there is thus evidence that liquidity commands a premium, possibly resulting from increased policy rates and reduced bank reserves. In addition, the somewhat wider spreads on lower-rated CP indicate compensation for credit risk (light versus dark red). In comparison, the compressed euro CP-OIS spreads suggest that liquidity is still abundant in the euro area, despite repayments on the ECB's targeted longer-term refinancing operations and its quantitative tightening. Likewise, the similarity of euro spreads across rating categories indicates little compensation for credit risk. Finally, the negative and wide CP-OIS spreads in the yen suggest that yen liquidity continues to be abundant, with investors willing to pay a premium to place their yen cash in bank-issued CP.

We also find that bank funding conditions tightened after the US debt ceiling impasse was resolved on 3 June. Namely, the average three-month OIS spread was almost 20 basis points higher for a period of about two months after 3 June compared with about the same period before ((Graph C1.B), dashed lines). This is consistent with investors expecting the debt ceiling resolution to tighten funding liquidity conditions in bank CP markets. This is because the resolution was expected to unleash heavy Treasury bill issuance, materially boosting the supply of low-risk instruments into the short-term funding markets where CP also resides. The effect was most noticeable for CP of the low-rated, A3 issuers (Graph C1.C), which tend to be the first to confront a change in funding conditions. The CP-OIS spread narrowed back in early August, in the wake of the surprise announcement by the US Treasury that new issuance will take place at the long end of the yield curve, which investors did not perceive as a substitute for CP.

* The views expressed are those of the authors and do not necessarily reflect the views of the BIS.

M Aquilina, A Schrimpf and K Todorov, "CP and CDs markets: a primer", BIS Quarterly Review, September 2023, pp 63–76. See, for example, D Gefang, G Koop and S Potter, "Understanding liquidity and credit risks in the financial crisis", Journal of Empirical Finance, vol 18, no 5, 2011, pp 903–14.